Most enterprises do not have a forecasting-model problem. They have a decision-confidence problem. When leaders ask whether ARIMA, Prophet, or LSTM is “best” for price prediction, they often start in the wrong place. In real enterprises, the winning model is not the one that sounds most advanced in a steering committee. It is the one that produces dependable forecasts, survives scrutiny, and improves commercial judgment when the cost of being wrong is high.

Executive answer

ARIMA is often the best baseline for enterprise price forecasting because it is transparent, fast to evaluate, and easier to govern. LSTM can outperform ARIMA when the data has enough history and meaningful non-linear structure, but that advantage is not consistent across datasets. Prophet is useful when seasonality, calendar effects, and business events matter more than deep pattern complexity. The practical lesson is simple: enterprises should choose the model that improves decision confidence under real operating conditions, not the model with the most technical prestige.

Why Forecasting Errors Now Carry Board-Level Consequences

In sectors such as plantation, energy, aviation, manufacturing, and the public sector, price forecasts shape procurement timing, contract exposure, budget ranges, inventory commitments, and margin assumptions. That makes forecasting less of a technical exercise and more of a control mechanism for the business. When prices move unexpectedly, the damage does not stop at forecast accuracy. It shows up in working capital pressure, weaker pricing decisions, and less credible management guidance.

That pressure has intensified because executives now operate in markets where volatility, event shocks, and structural breaks are common. A model that looked stable in the last planning cycle can deteriorate quickly when the market changes regime. That is why leaders should care less about whether a model can generate a forecast and more about whether the organization can trust that forecast enough to act on it.

Why Many Teams Assume the Most Advanced Model Must Be the Best Model

The common assumption is that complex price behavior requires a complex model. That belief explains why LSTM and other deep learning approaches are often treated as the natural next step once a team decides it wants to be “serious” about forecasting. It sounds logical. If markets are non-linear, then a non-linear model should win.

The problem is that the evidence does not support a universal hierarchy in which deep learning simply replaces traditional statistics. A large comparative study published in PLOS ONE found that popular machine learning methods were outperformed by traditional statistical methods across multiple forecasting horizons on 1,045 monthly series, while also requiring greater computational effort. The M4 competition reached a similarly inconvenient conclusion: among the most accurate methods, the strongest performers were largely combinations of statistical approaches, while pure machine learning methods performed poorly overall.

That does not mean LSTM lacks value. It means leaders should be wary of a procurement mindset that treats complexity as proof of superiority. In enterprise forecasting, sophistication is only useful if it translates into repeatable, measurable advantage.

Why That Assumption Breaks Down in Real Enterprise Forecasting

The first problem is evaluation discipline. Many teams compare models using a narrow test window or a single accuracy metric, then declare a winner too early. Hyndman and Koehler showed that common forecast-accuracy measures can be misleading, degenerate, or undefined in ordinary business settings, particularly when data includes zeros or problematic denominators. They proposed MASE as a stronger measure for comparing forecast accuracy across series, while the PLOS ONE study used both sMAPE and MASE because a single metric can distort the conclusion.

The second problem is enterprise operating reality. LSTM can detect non-linear relationships, but it also demands more disciplined data pipelines, more retraining rigor, and more tolerance for opacity. That becomes inconvenient when the forecast must be explained in an executive review, defended after a miss, or recalibrated quickly when the market changes direction. A model that cannot be governed confidently is not automatically a better enterprise model just because it performs well in a narrow experiment.

The third problem is generalization. One study can show LSTM beating ARIMA convincingly, while another shows the reverse. That is not a contradiction. It is a reminder that forecasting performance is conditional on data structure, time horizon, and evaluation method. Enterprises that ignore that condition usually end up overpaying for complexity or underinvesting in strong baselines.

The Better Question: Which Model Improves Decision Confidence, Not Just Accuracy Scores?

The right framing is not ARIMA versus LSTM. It is fit for decision-making versus fit for demonstration.

That sounds subtle, but it changes how leaders should evaluate forecasting choices.

A board-ready forecasting approach should be judged on four dimensions:

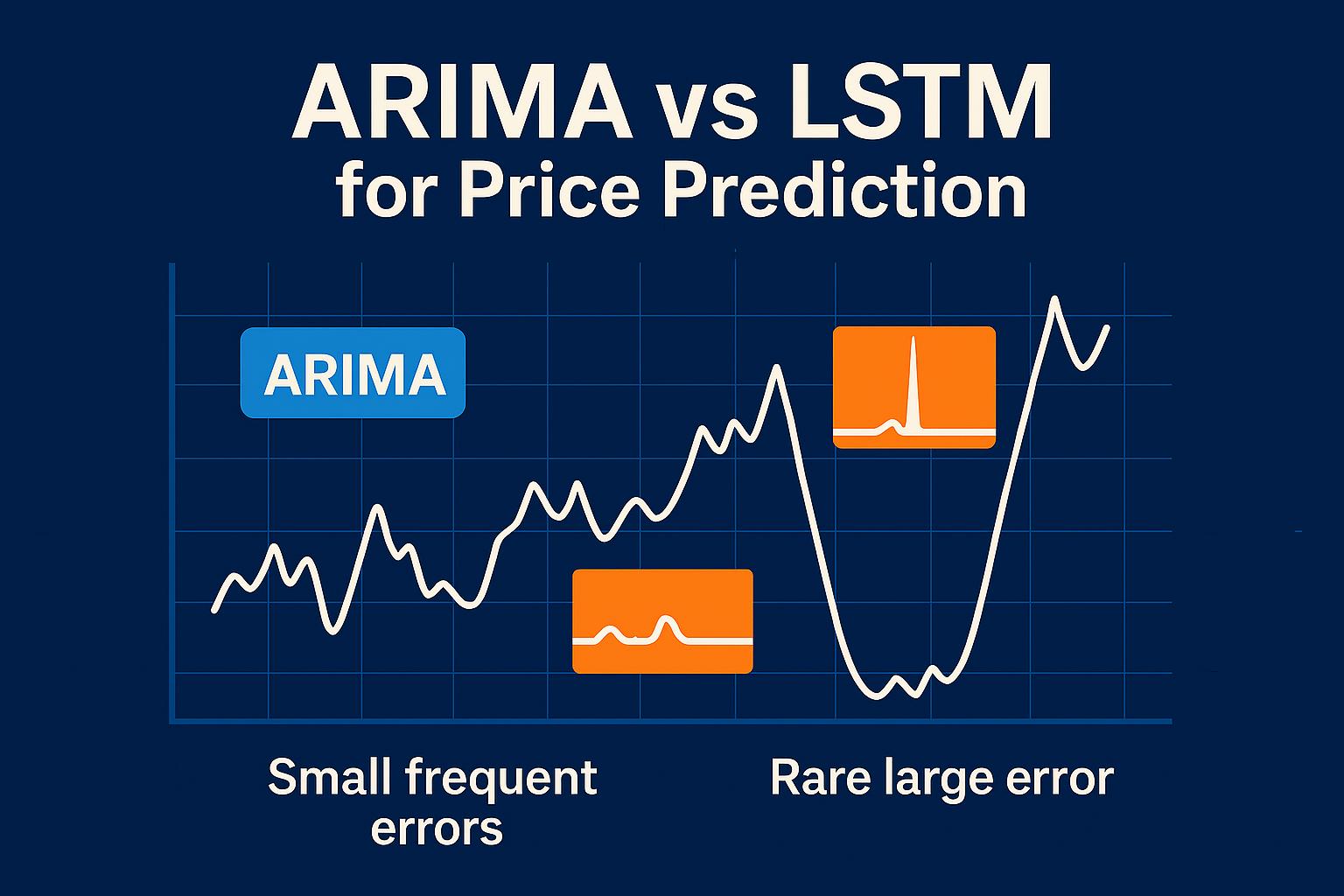

- Error economics: which type of miss hurts the business most—small frequent misses or rare large ones?

- Data regime: how much stable history exists, and how often do patterns break?

- Governance burden: can the output be explained, challenged, and improved without specialist dependency?

- Operational resilience: does the model remain useful when data quality weakens or the market shifts?

Under this lens, model selection becomes less ideological. ARIMA is attractive because it is interpretable, efficient, and often strong on structured short-to-medium horizon forecasting. Prophet is attractive when trend shifts, seasonality, and calendar effects dominate the signal. LSTM becomes attractive only when the organization genuinely has enough data, enough non-linearity, and enough operational maturity to justify the extra complexity.

How CEOs, CFOs, and CTOs Should Evaluate ARIMA, Prophet, and LSTM Differently

When ARIMA is the right control model

ARIMA should be the statistical control model in almost any enterprise forecasting exercise. It remains useful because it is transparent, fast to retrain, and often highly competitive against more complex alternatives. In the PLOS ONE comparison, statistical methods outperformed machine learning methods across multiple horizons, and ARIMA was included precisely because it remains a serious benchmark in practice. In a 2025 study of Indonesian banking stocks, ARIMA also outperformed both ARIMA-GARCH and LSTM across all equities, recording average MAE 74.46, RMSE 93.01, and MAPE 1.297%.

For executives, that matters because ARIMA offers a defensible baseline. If a more complex model cannot beat it consistently under rolling evaluation, the burden of proof remains with the complex model, not with the baseline.

When Prophet earns a place

Prophet is most useful when price behavior is materially shaped by calendar effects, recurring seasonality, and trend changes that business teams can recognize and explain. It is not a universal replacement for ARIMA or LSTM, but it can be effective in event-heavy contexts. In a 2024 peer-reviewed study on antidiabetic drug demand forecasting, Prophet achieved MAE 0.74, outperforming SARIMA at 2.18 and ARIMA at 3.02, which suggests clear value when structured seasonal behavior matters.

For enterprise leaders, Prophet is less about fashion and more about suitability. If your series behaves like a business calendar before it behaves like a neural network problem, Prophet deserves consideration.

When LSTM is justified

LSTM becomes credible when the organization has long enough history, enough signal complexity, and enough discipline to manage model drift. In a 2025 study on the DAX 50 ESG index, LSTM achieved lower MAE, RMSE, and MAPE than the best ARIMA model in both static and expanding-window evaluations, though the paper described the advantage as statistically significant yet modest. In a separate 2025 crude-oil forecasting study, bidirectional LSTM outperformed ARIMA with RMSE 91.36 versus 266.64, MAE 67.487 versus 225.35, and MAPE 19 versus 43.

The executive reading is clear: LSTM can win, but it does not win by entitlement. It must earn its place through data fit, rolling evaluation, and governance readiness.

Which Error Metrics Matter: MAE, RMSE, MAPE, and MASE

MAE is useful when leaders want error expressed in the same unit as the business variable. It is intuitive and easy to explain in operating reviews. RMSE matters when large misses are especially costly because it penalizes large errors more heavily. MAPE is easy to communicate as a percentage, but it can break down when actual values are zero or very small. That is why Hyndman and Koehler argued that MASE is often a more reliable way to compare methods across multiple series.

The practical discipline is to avoid single-metric decisions. If a model wins only on one measure and loses on others, leaders should understand what that means economically before adopting it. Forecast evaluation is not a beauty contest. It is a controlled test of business usefulness.

What the Evidence Shows About ARIMA vs LSTM in Real Forecasting Contexts

Across the available evidence, three patterns stand out.

First, no single model family wins everywhere. LSTM outperforms ARIMA in some financial and commodity studies, while ARIMA remains stronger in other financial datasets. That alone should end the habit of choosing a forecasting method by reputation rather than evidence.

Second, simpler methods remain remarkably competitive. The M4 competition and the PLOS ONE benchmarking work both show that statistical and hybrid approaches remain highly effective, and that pure machine learning does not automatically deliver superior forecasting performance.

Third, hybrids often outperform purists. In the M4 competition, one of the biggest surprises was a hybrid approach that blended statistical and machine-learning elements and delivered roughly 10% better accuracy than the combination benchmark. That result matters because it suggests the best enterprise answer is often not a philosophical choice between old and new, but a disciplined combination of both.

What This Means for Margin Protection, Planning Credibility, and Executive Decisions

For CEOs and CFOs, the forecasting question is ultimately financial. Which model reduces exposure to bad timing, poor pricing decisions, and unreliable planning assumptions? For CTOs and CDOs, the question is organizational. Which model can be deployed, monitored, explained, and improved without becoming fragile or dependent on a small specialist team?

The answer, in most cases, is not to start with the most complex option. It is to build a forecasting hierarchy. Begin with a strong statistical baseline such as ARIMA. Test Prophet where business seasonality and events matter. Escalate to LSTM only when the data regime, evaluation results, and governance maturity clearly justify it. This approach improves not only forecast quality, but also executive confidence in the decisions built on top of the forecast.

Executive takeaway

The best forecasting model for enterprise price prediction is rarely the most fashionable one. It is the one that consistently beats a transparent baseline, performs well across the right error metrics, and remains governable under real operating conditions. ARIMA should be the control. Prophet should be used where seasonality and business-event structure are real drivers. LSTM should be approved only when the organization has both the data and the discipline to support it. In board terms, the issue is not model sophistication. It is decision confidence.

FAQ 1

Is ARIMA or LSTM better for price prediction?

Neither model is universally better. ARIMA often performs well when the data is relatively structured, the history is limited, and explainability matters. LSTM can outperform ARIMA when the dataset contains enough history and meaningful non-linear patterns, but multiple studies show that this advantage is inconsistent across markets and forecasting contexts.

FAQ 2

Why do enterprises still use ARIMA if deep learning models exist?

Because ARIMA is often easier to trust, govern, and benchmark. Traditional statistical methods have remained highly competitive in large forecasting comparisons, and they usually require less computation and less operational complexity than machine learning alternatives. For enterprise leaders, that makes ARIMA a strong control model before approving more complex approaches such as LSTM.

FAQ 3

When should a company use LSTM instead of ARIMA?

A company should use LSTM only when the data genuinely supports it. That usually means a longer and cleaner time-series history, evidence of non-linear behaviour, and a team that can retrain, monitor, and explain the model over time. Even then, LSTM should be approved only after it consistently beats ARIMA under rolling or expanding-window evaluation, not just on a single test split.

FAQ 4

What error metrics matter most when comparing ARIMA and LSTM?

The right metrics depend on the business decision. MAE is useful when leaders want errors expressed in business units, RMSE matters when large misses are especially costly, and MAPE is easy to communicate but can become unreliable when actual values are zero or very small. That is why Hyndman and Koehler recommend MASE as a stronger comparison metric across multiple series.

FAQ 5

What is the best forecasting approach for enterprise price prediction?

The best approach is usually a disciplined model hierarchy, not a single model bet. Start with ARIMA as the baseline, test Prophet where seasonality and calendar effects are important, and use LSTM only when the data regime and evaluation evidence justify the added complexity. Broad forecasting evidence also suggests that hybrid and combined methods often outperform purely statistical or purely machine-learning approaches on their own.